We Are Looking at a Hawkish FOMC that Won’t Cut in December

Fed funds futures overestimate December cut odds. Regional Fed presidents have turned hawkish after hearing inflation concerns from business leaders. Tariffs aren't transitory, and the Fed's suddenly worried about missing its 2% target for 5 years. Expect rates to hold.

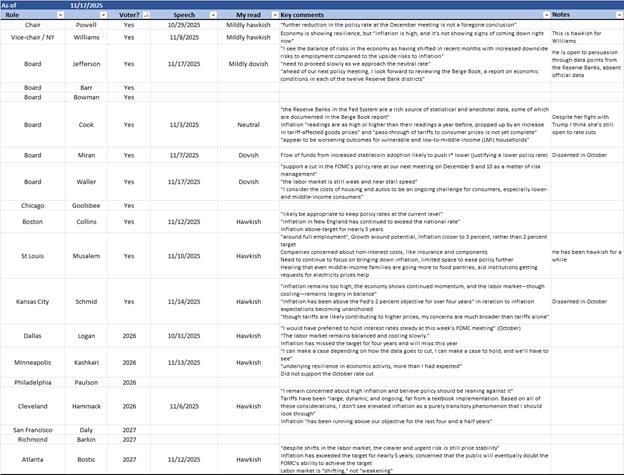

I've been tracking FOMC member speeches and the shift over the last two weeks is striking.

Fed funds futures prices currently imply about a 50% probability of a rate cut at the December 10 FOMC meeting. I think this is overstating the odds of a cut. This is understandable, because this is a Committee that has become hawkish, and very suddenly, and the market is still in the process of catching up.

Here is my latest FOMC matrix, followed by my top 3 takeaways.

#1 – The regional Reserve Bank presidents are all hawks

All of the regional Fed presidents that gave speeches after October 29 are hawkish.

Out of this bunch, Musalem/St. Louis has been the most hawkish, at least since September. Beyond Schmid/Kansas City’s dissent arguing against a rate cut at the October meeting, what surprised me the most were the comments from people like Logan/Dallas, Hammack/Cleveland, and Kashkari/Minneapolis all saying that if they had a vote, they would have voted against a cut.

Logan, Hammack and Kashkari are all rotating in as voting FOMC members in 2026. The fed funds futures market is currently pricing in about 3x 25 basis point cuts over the coming 12 months. I don’t see these three voting for three cuts unless we get significant progress on inflation moving back to 2%, or we see significant deterioration in the labor market over the coming year.

Why are they so hawkish, in comparison to the Board? I think this comes down to the regional Fed presidents spending more time in the community with local business leaders. The regional Fed presidents are hearing every day about inflation pressures in direct conversations. (We’ll read this anecdotal evidence in the next Beige Book.) By contrast, the Board of Governors is in Washington D.C., and its members are less connected to conditions on the ground.

#2 – Tariffs are not “transitory”

Hammack said that tariffs have been “large, dynamic, and ongoing, far from a textbook implementation. Based on all of these considerations, I don’t see elevated inflation as a purely transitory phenomenon that I should look through.” She also said that business leaders in her district have been telling her that they have no choice but to raise prices in Q1 of next year. Musalem made a similar point in September.

The FOMC’s decision to “look through” tariffs, because the economics textbook says they are supposed to be a one-off shock, rests on 1) the full effect of tariffs already being realized and 2) no more tariffs being added. Musalem and Hammack are being told directly that 1) isn’t true, and we all know that 2) isn’t something you can bet on.

#3 – Everyone is suddenly talking about missing the inflation target for 5 years

Do you have your tinfoil hat nearby? Yes? Great, put it on.

Schmid, Logan, Hammack, Bostic, and Collins (all Reserve Bank presidents) all said something to the effect of “inflation is above our target and has been for nearly 5 years.”

Why are they suddenly talking about missing the target for 5 years? Why didn’t it worry them when we were missing the target for 4.5 years, or 4 years straight?

In the speeches, a handful of them said that they are worried about longer-term inflation expectations (which remain stable, a point made by Waller in advocating for a cut in December) becoming unanchored. Essentially, the public (and the market) currently believes that the FOMC will succeed in getting the inflation rate back down to the 2% target. But if the FOMC misses the target long enough, the public will stop taking them seriously. This is a problem because inflation can become a self-fulfilling prophecy—if I believe that inflation will be high next year, then I raise my prices in anticipation of that, and my customers raise their prices in response, and that becomes an inflationary spiral. So that’s the argument.

But I don’t think that’s the whole story. This sudden hawkish commentary feels coordinated to me—aside from Musalem, who's been consistent. I think the Democrats winning three off-cycle elections—the governorships of New Jersey and Virginia, and the mayoral race in NYC—caught people’s attention. Although the winning candidates included both centrists and the far left of the Democratic Party, all of them campaigned on cost-of-living issues. President Trump certainly got the message, as he announced the removal of tariffs on coffee, beef, and some other agricultural products days later.

I think the Reserve Bank presidents all got the message too, and unusually they are all singing the exact same tune. Added to the direct concerns on inflation they are hearing from local business leaders, this is a group that realizes inflation is still a big problem. Bowman’s argument that if you back out 40 basis points from the tariff impact, and then you round down, we’re basically at 2 percent, isn’t good enough.

Whether driven by political awareness, business feedback, or both, I expect the Committee to hold rates steady in December.